View from the highway that caught my interest. That is a lot of wells. Photo by James Ulvog.

One of many ways energy wizards are driving down the cost of drilling for oil is putting multiple wells on one site.

7/4 – Amy Dalrymple at Dickinson Press – Bakken multi-well pads getting bigger– The technique of drilling several wells from one site, called multi-padmulti-wellpad drilling, is increasing. Both the number of pads and the number of wells per pad is going up.

For several years now I have noticed multiple pump jacks on one site.

In September 2015, I saw a 15 well pad. It is a few miles west of Ross and about a mile and a half north of highway 2. You can see it on Google maps at coordinates 48.333785, -102.653962, although the satellite photo is really old. It shows only the middle six wells with pumps installed and a drilling rig working on the west row of wells. No progress on the east row of wells.

One more illustration of the energy revolution currently underway. BTW, flaring is down to 9.2% of all natural gas produced. About 91% is captured, which shows great progress. Photo by James Ulvog.

When I look at the political news and the headlines in general news every morning, I get so discouraged. When I look away from those areas I am so optimistic.

Consider what the two following articles suggest about how bright our economic future could be: an abundant supply of oil and gas at increasingly lower cost to produce.

6/13 – JH at The American Interest – Resilient Shale Producers Get Their Second Wind – Article mentions a Financial Times article which indicates there is some increase in drilling, which is driven by prices a few weeks ago. Since then oil prices have come up further. Discussion speculates if prices remain in the $50 range there will be even more drilling.

The small-scale and short development time of shale wells creates a soft ceiling on prices. Shale production can increase quickly which will put supplies on the market quickly, which will counter a surge in prices.

A quoted analyst says his expectation is a long-term price of oil around $60. There will be fluctuations up to $80 and down to $40, but the price will tend toward $60. Drillers needing a price higher than that to be profitable will have a rough time.

6 pumpjacks in Sept. ’15 about ready to get working. Photo by James Ulvog.

Lots of transitions going on in the oil industry, particularly Saudi Arabia. I have a bunch of articles to discuss on energy. Will try to get caught up.

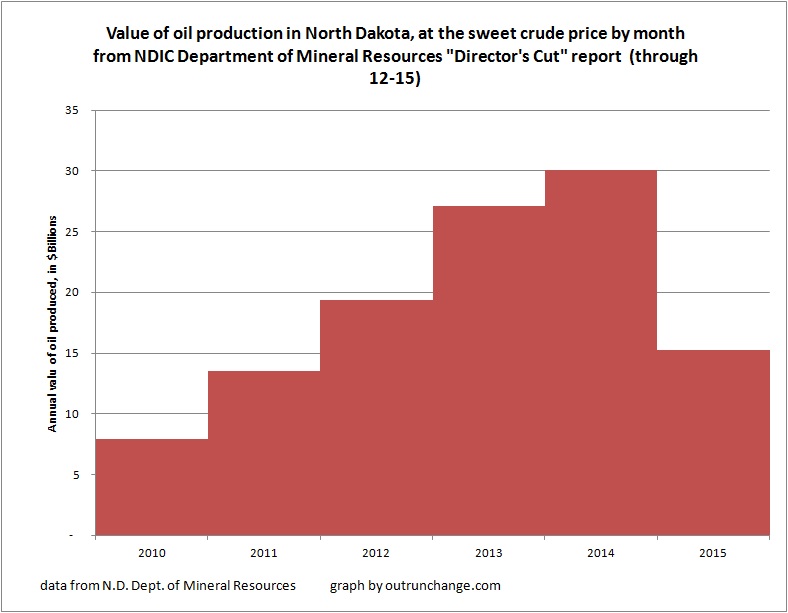

Some graphs to show the value of oil produced in North Dakota.

First, the value of production by year from 2010 through December 2015.

To show the impact of volume, next is a graph of the volume of production for the year from 2003 through 2015.

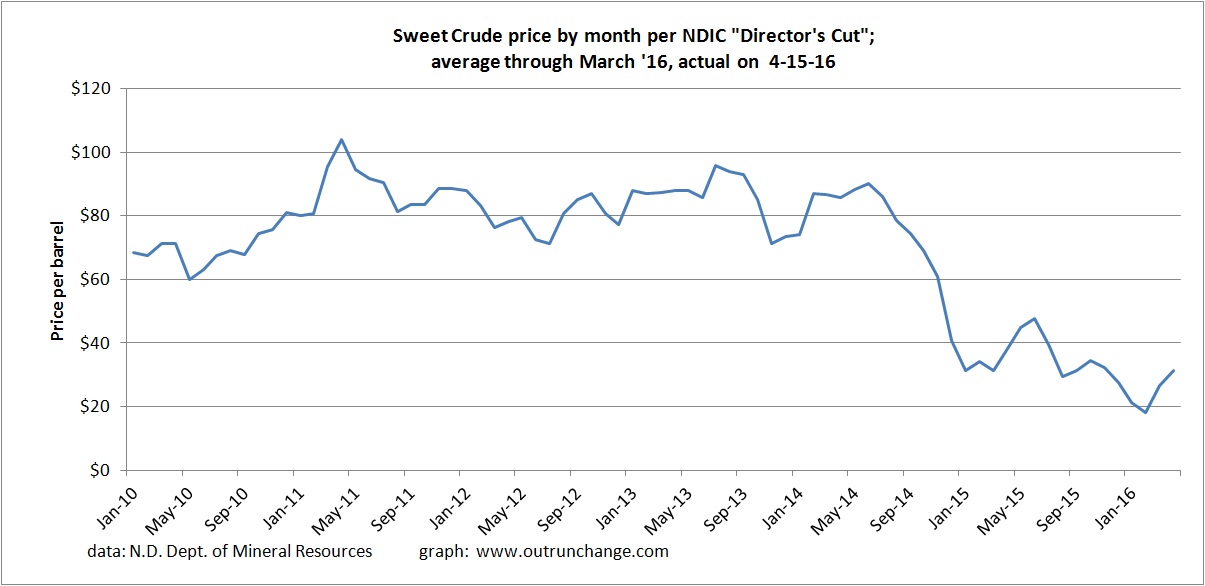

Finally, to see the impact of drop in prices is a graph of the value of monthly production from January 2010 through February 2016. Based on information through mid-April, February was the low point in oil prices. There has been an uptrend since then.

Horizontal drilling and hydraulic fracturing have turned the energy world upside down. The massive transition isn’t over. A few articles on the massive benefits of fracking. Part 1 of this discussion here.

Pointing out news that is not news to anyone who has paid attention to the energy business in the recent years, article explains the current volatility is currently disrupting and will continue to disrupt many producers. A lot of producers will go out of business. Keep in mind that the drilling rigs, equipment, and especially the oil under the ground will not vaporize as a result. The know-how to more efficiently drill more productive wells more quickly more cheaply will be around a long time.

Article explains a cited book which makes the point that the shale revolution is just getting started. The improved efficiency producing higher output in the last two years has brought many producers to the point where they can be productive in the $30 or $40 range.

The technology has increased to the point that if prices rebound to slightly higher levels than where they are now would make it possible to bring horizontal drilling and hydraulic fracturing into conventional oil fields and produce increases there.

The net effect of all these amazing advances is that shale oil will put a cap on how far oil prices can rise. As prices go up a whole bunch of undrilled locations become lucrative.

My rough graph above shows the lousy accuracy of Dr. King’s 1956 projections of natural gas production in the US.

Dr. M. King Hubbert fell in with a fellow named Howard Scott, whom Prof. Priest calls

a magnetic charlatan.

Mr. Scott dreamed of a glorious time in which scientists and engineers would run the world through a powerful Technate or Technocracy Inc. As I havementioned before, I’m not sure if this authoritarian system was more fond of fascism or communism, but it certainly was authoritarian. My inclination is this tended toward fascist, meaning our betters would let us peons own private property but they would tell us what we can do with our property and how we can live.

Dr. King was apparently not a very nice person. The review highlights Dr. King’s approach to knowledge:

It was not enough for him to be right. Someone had to be humiliated in the process. Mr. Inman appears uninterested in pondering the mixture of arrogance and resentment that shaped Hubbert’s personal interactions.

That Dr. King had an overabundance of arrogance is visible if you read through his 1949 and 1956 papers.

Horizontal drilling and hydraulic fracturing has turned the energy world upside down. The massive transition isn’t over. A few articles on resilience of the industry.

Oh, and a university report showing no ground water contamination from fracking will be kept from public view. Why? Actual research results contradict the researcher’s stated agenda.

How much new housing will Williston need in the next few years? None? Some? A lot? Photo by James Ulvog.

A recurring human foible I see is making an assumption that the immediate past trends will continue in a straight line forever.

In the context of crude oil in general and western North Dakota in particular, the question is whether the slump of the last year will continue for an indefinite period of time (measured in years or even decades) or will there be surges in production at various points?

City officials in Williston give every indication of thinking that the boom is over and will never return. Seems like they are preparing for life in the city and surrounding area to have current level of employment plus only slow growth for decades.

I think that reasoning is why there is opposition from public officials to expanding the airport. Why spend any money on a new airport when you don’t need the extra capacity this afternoon and for the rest of the week? There is no reason to go through all the effort of tearing up farmland when the current airport is sufficient for traffic this month. There are open seats on flight to Minneapolis. Why, I’ll bet the airlines could even add a flight or two if they actually get more customers.

Why not chase all the crew camp facilities out of town? They are not needed. There is enough capacity in apartments and hotels to absorb the number of people who are in crew camps this month, so what purpose is there for ever again having any crew camp capacity in the city? Just force the temporary workers who don’t know how long they will be in the area to sign a one-year lease and everything will be fine. In the alternative, they can just stay in hotel that will only cost $3,000 or $3,500 or more per month. Problem solved.

If you assume that oil prices will stay where they are today for the next several decades and if you assume the number of rigs in North Dakota will stay in the range of 20 or 30 or 40 for a decade or two then you should plan for a city with population at about the current level.

If you assume the trends of the last 12 months will continue for decades, then there is no need for new facilities.

Rounding out the picture of North Dakota oil production based on data released by the state on April 15, 2016, here is a graph of the sweet crude prices in North Dakota from January 2010 through April 2016. Quite visible is the dramatic drop in late 2014. Of particular note is prices have recovered in the last two months.

Next is a graph of the rig count by month. You can also see a dramatic drop starting the end of 2014.

Finally is a graph of the fracklog from January 2012 through February 2016. This is the number of wells that have been drilled yet are uncompleted (DUC) meaning the well is drilled to total depth but the fracking has not yet been done. Basically this is a half million barrels of oil put on the inventory shelf until prices recover. That represents nearly a thousand wells than can be brought on-line rather quickly.

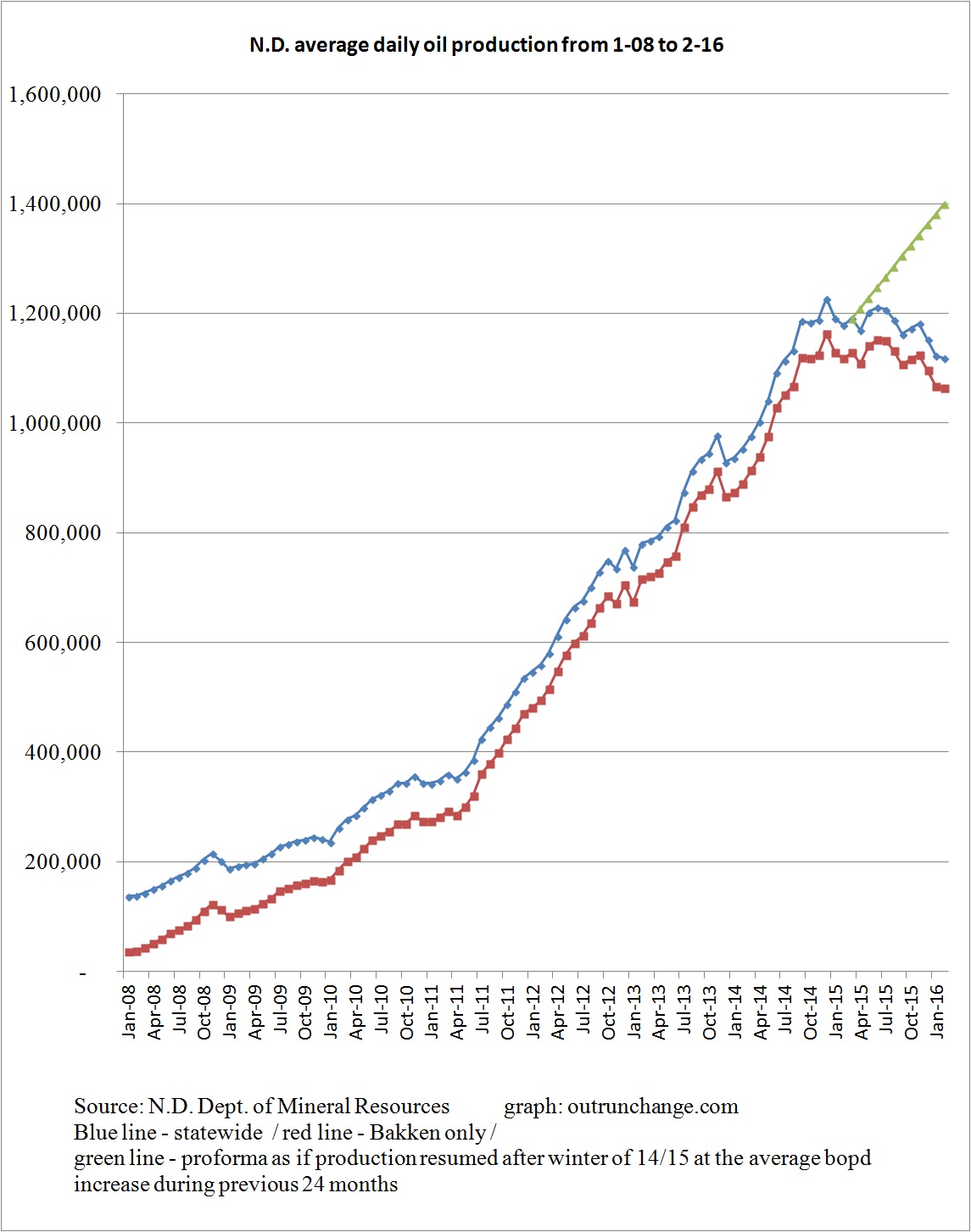

Average daily production dropped to 1,118,333 bopd (Prelim) in February from 1,122,462 (revised +352 bopd) in January. That is a mere 4,129 bopd decline, or 0.37%.

Here are a few graphs to paint the story. First average monthly production from 2008 through February 2016 showing total for the state and Bakken field only. Included in that graph is a pro forma of what production would have been (based on my wild guess) if the production increased after the winter at the average rate of increase over the preceding 24 months.

Second graph is average production in the state since 1990. Finally, to show the change since 2010 more dramatically is a graph of production since 2004.

Will we see bunches of those soon? Yes, no, maybe so.

Will production of shale oil recover as oil prices rise? I’ve seen several articles discussing whether that can or will happen. Three articles saying yes, no, and maybe so.

Continental Resources says will start drilling if US crude increases to mid $40 range. Whiting Petroleum will start completing DUC wells if oil is in the low 40s. A year ago comments were that companies would start increasing the drilling if oil hit $70.

Article says Hess reduced the cost of a new well by 28% over the last year.

EOG says they have these rights for 3,200 wells which would produce a rate of return of 30% when oil is at $40.

Implication of these comments is shale production would likely ramp up when prices move into the 40s, perhaps more likely the high 40s. That would create substantial pressure on worldwide oil prices, keeping them from rising too far.

No.

3/15 – Wall Street Journal – Many Shale Companies Are Unable to Ramp Up Oil Output – Article raises a great point that just as output from shale oil has fallen slower than anyone expected, there are different reasons that shale producers may be challenged to ramp up production when prices increase.

Here is a recap of the North Dakota rig count, all from Million Dollar Way. Also, an article quantifying the impact on employment from the drop in rig count.

Fascinating to watch news in February about OPEC’s strategy. First, IEA sees a drop of US shale oil in 2016 and 2017 with strong growth in output over the following four years.

I have quite a backlog of lot of articles on energy to discuss. Will try to get caught up. Here goes…

Article at the end of January indicated OPEC is publicly claiming things are going swimmingly well. Then Saudi Arabia and Russia agreed to freeze their production at the January level, which is near record level of output for both countries. Then the end of February OPEC’s secretary-general acknowledged that the intentional goal was to wage a price war against US shale. Also acknowledged the price war hasn’t worked like they planned.

I don’t think that crippling the Russian, Saudi Arabian, and Venezuelan national budgets by dropping prices about 60% with no near-term expectation of recovery is quite what they had in mind.